Why jet engines aren't made in China

Why Jet Engines Aren’t “Made In China”

What China’s jet engine program tells us about the limits of industrial policy

In my recent article contrasting Chinese dynamism with American sloth, I described how the Chinese state-capitalist system has an unusual tolerance for social disruption, which, when paired with prescient leadership, enables massive societal uplift. Many of the comments, however, extrapolated this observation about state capacity into prophecies of inevitable American decline that I did not intend to imply. Perhaps the slight polemical detour gave some of the audience license to veer towards doomerism.

So let’s be clear: this is an incorrect assumption. A united Western alliance possesses many structural advantages the Chinese state will struggle to replicate. Instead, I think China-hysteria is largely just a belated overcorrection. After two decades disparaging the idea that any other power could pose a challenge to Western hegemony, we’re now astounded by the very existence of competition. But this overreaction blinds us to nuance.

China is not a national wunderkind: it is a technologically-advanced state that has an extraordinary capability to marshal national resources. Most of its successes involve utilizing this advantage to scale a mature technology, become its dominant provider, and use the synergies that affords to expand horizontally and vertically. This strategy finds success in some industries but meets with failure in others. The pattern of where it fails is informative.

One illustrative example of failure is in jet engines. China has tried and failed for some fifty years to produce military and commercial jet engines at parity with the West. Why did it fail? Because, as I explore below, jet engines are almost uniquely designed to expose the weaknesses in the Chinese system. They’re a low-margin market focused on long-term reliability where manufacturing quality and consistency are paramount. Iteration speed is very slow and there’s a pervasive, internationally enforced, regulatory barrier for every finished product. These together neutralize the usual Chinese advantages in skilled labor, capital, and speed-to-scale. They also prevent traditional domestic protectionism from adding much value.

Analyzing the Chinese failure to produce viable jet engines gives us important lessons about the nature of the West’s remaining comparative advantage.

Turbine Blades As A Microcosm

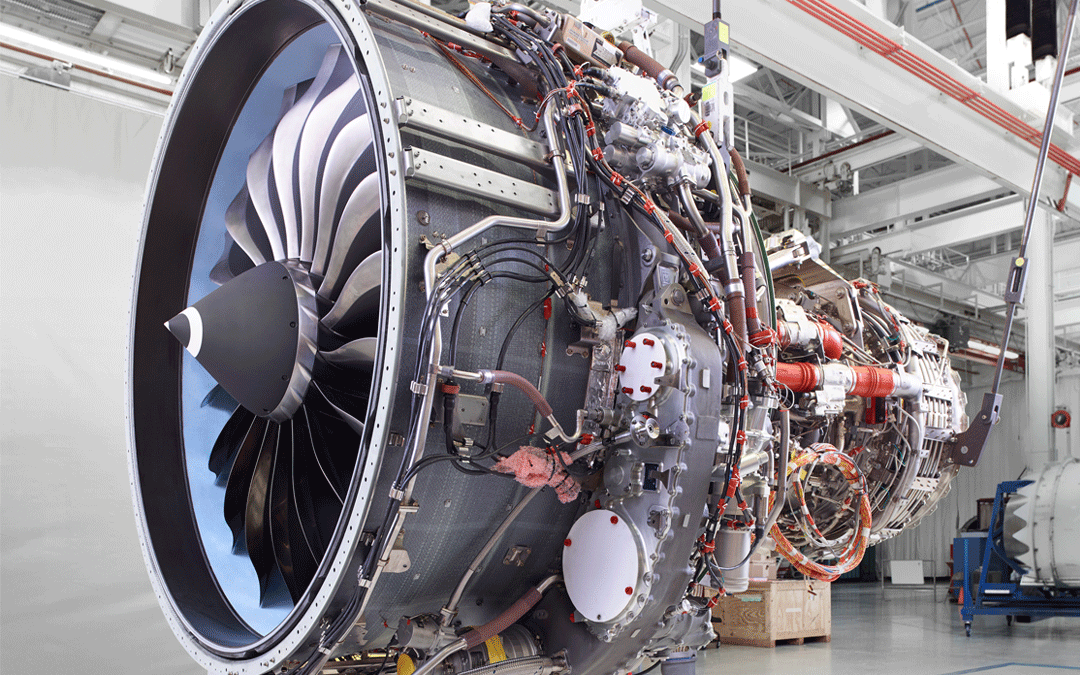

A high-pressure turbine blade in a modern jet engine is expected to sit in gas hotter than lava, rotating faster than the maximum redline of a Formula One engine, while sustaining a consistent centrifugal load heavier than a Ford Focus. And it’s expected to do this without stretching, melting, or cracking for 30,000 hours-about 4 years-of continuous flying time. A failure in these blades would be catastrophic, resulting in the destruction of the engine, likely followed by the plane itself.

Achieving these requirements has made it one of the most complex manufacturing outputs in the world. The initial challenge comes from fabricating the material. Frank Whittle’s first jet engines used Nimonic-75: a nickel-chromium-titanium alloy that crept (i.e. elongated under stress) over 700C, with a service lifespan of only for tens of hours. The breakthrough came in the late 1940s, when a British metallurgist realized that adding more titanium and some aluminum produced dramatic strengthening. This yielded Nimonic-80A, which is the base of every subsequent superalloy.

Each subsequent generation then added new elements to the mix to solve the previous generation’s failure modes. Second-generation alloys added rhenium for creep resistance, a metal so rare its annual world production is fifty tons. Third-generation alloys doubled the rhenium content, which improved temperature capability but created brittleness under load, so the most recent iteration adds ruthenium, an ever rarer metal only produced as part of South African platinum mining.

The other major challenge is casting. Molten metals do not cool uniformly. Instead, different parts of the metal solidify at the same time, and these simultaneous solidification processes form multiple crystals in the final solid. These crystals meet at grain boundaries. Historically, the most common failure mode for a turbine blade is a fissure along these grains. To mitigate this, the modern turbine blade is cast using the single-crystal method.

Developed in the 1980s, this method maintains a uniform temperature gradient along the molten metal’s surface to pull solidification in one direction, and combines that with a grain selector, a helical “pigtail” shape in the caster that compresses the solidifying metal to ensure that only a single nucleation process succeeds. This creates a final metal that has no grains at all.

The biggest complication here is yield. During the single-crystal casting process, dozens of variables need to be maintained within very small tolerances. Any disturbances during the process, any imperfections in the base material, any trace dissolved gases during nucleation, and you have micro-grains that cause the blade to fail certification. Established manufacturers still only reach 50-70% yield; a new entrant would be in the low tens for years.

Consequently, there are only seven companies in the world that can build turbine blades at scale. First are the three main engine manufacturers:

- General Electric, with casting facilities in Quebec and South Carolina

- Pratt & Whitney in Connecticut

- Rolls Royce in Bristol, UK

The other four are specialty manufacturers:

- Howmet Aerospace in Michigan

- PCC Airfoils in Ohio

- Consolidated Precision Products in California

- Doncasters, a British company with plants in the UK, Germany, and Alabama

Each of these companies relies on a deep network of suppliers. The alloys are produced by four companies across the US, who source the elements from around the world. Ceramics are sourced from two companies: CoorsTek in Colorado or Morgan Materials in the UK. Injection dies come from Japan, Germany, or Switzerland. The Bridgman furnaces to cast the blade are built by four companies: ALD in Germany, Consarc in New Jersey, Retech in California, and ECM in France. Coating is sourced from companies in the US, Switzerland and Germany. And finally, inspection and certification equipment is a broad category coming from a swath of companies in Japan, the US, Germany, and the UK.

All in all, a single turbine blade contains products from some 100 different companies, spread across 25 different US states and 15 different countries. And turbine blades, as complex as they are, form just one component of a jet engine. A complete engine has over 40,000 parts, each of which operates under similarly extreme conditions that stretch the boundaries of conventional fabrication, and consequently, has its own exotic material composition and manufacturing process, optimized through decades of continuous engineering effort.

This creates a final product that is dependent on a massive horizontal network of suppliers, with production centered in the US, the UK, France, and Germany and raw minerals sourced worldwide. In the modern day, the largest engine manufacturers are Rolls-Royce, General Electric, Pratt & Whitney, and Safran, who, through various joint ventures, produce the vast majority of the most advanced commercial and military jet engines in the world.

This is a longstanding equilibrium. For the past half-century, these four companies have powered most aircraft produced in the world. The major notable exception is the Soviet Union/Russia’s domestic industry, which has consistently remained a decade behind the West. But there is another-far smaller-player in the industry: China.

Since 1986, when Deng Xiaoping established a strategic imperative for indigenous jet engine production, China has invested hundreds of billions in creating their own, parallel industry. This mirrors a massive outgrowth in Chinese investment in all sectors, in service of China’s nebulous goal of “strategic autonomy”-better known in the west as autarky. And in most industries, China has had unadulterated success.

China’s vast pools of high-skilled labor and near limitless state-provided capital have allowed it to take over each technological frontier, squeezing out incumbent players. Notable examples here are electric cars, renewable energy, electronic components, and mature-node semiconductors. This pattern of Chinese industrial dominance has become so consistent that the West almost deems it prophecy.

It may be surprising, then, that in jet engines, China remains at least a full decade behind the West. Even after forty years of state-directed investment, China’s flagship commercial jet, the C919, is still powered by the LEAP-1C, made by CFM, a GE-Safran joint venture. China’s prospective competitor, the CJ-1000A, has faced numerous delays, and is now not slated to enter production until at least 2030. Meanwhile, China’s first fifth-generation fighter, the Chengdu J-20B, relied on a thirty-year old Russian AL-31 for a full decade until its domestic WS-15 program, which was started in the 1990s, was deemed ready for production. Even then, it’s projected to be far behind the Pratt & Whitney F135, the F-35’s engine, in durability, reliability, and efficiency. Its other fighter uses an outdated, 20-year-old Chinese engine.

Indeed, China, which has otherwise mastered the catch-up growth formula, and has built a massive bank of manufacturing talent and capital, has not managed to produce any asymmetric speedup in jet engine manufacturing. The frontier remains clearly western. Why? Because China’s most visible successes-the ones we cite most often when we ruminate on the “death of Western dynamism”-have broadly similar market structures. Jet engines are notably distinct.

China has excelled in industries with legible technological targets, well-known manufacturing processes, and fast iteration cycles. Their strategy has been to choose technologies with mature fundamentals but underserved demand, and then deploy capital to scale up production very quickly. These industries have fast iteration cycles, allowing Chinese companies to rapidly improve their designs, while their scale allows them to undercut Western manufacturers on price and quantity. The Chinese state helps this along by protecting nascent industries from foreign competition, giving them a domestic market to expand in before moving into exports. Together, these factors allow Chinese firms to define a new, much lower floor in the market which they can own entirely. This allows them to accumulate knowledge and optimize their manufacturing process, eventually enabling them to move upmarket into higher-margin segments where they compete directly with Western incumbents.

The jet engine is the antithesis of each of those properties. Reliability targets are not like battery range or solar panel yield. They depend on alignment between every component in an engine, making them hard to directly optimize for. Iteration speed is very slow because reliability is very difficult to know a priori: it requires extensive testing and real-world monitoring. And jet engines do not have any lower-tier market with underserved demand: there’s a small set of customers with very strict requirements and a mature set of incumbents to supply them. China’s jet engine program is stuttering because it’s applying a scale-focused method to an industry where the moat is accumulated knowledge.

Where China Succeeds

The most illustrative example of Chinese catch-up growth is its domination of electric vehicle production. China started building EV capacity in 2009, when Tesla was still a limited-capacity luxury brand and Western manufacturers were focused on building hybrid cars to preserve the value of their internal-combustion engine investments. Chinese manufacturers thus entered a wide-open market without any real incumbents. They were starting fresh-they didn’t need to retool their workforce or rebuild their factories.

Electric vehicles are also considerably easier to manufacture than gas cars. Instead of 2,000 part internal-combustion engines built on decades of mechanical engineering expertise, with transmissions, fuel injection, and emissions controls, electric cars are driven by a single commoditized component: the brushless motor. The Chinese state helped them along by creating domestic demand, where Chinese citizens were given expansive subsidies to buy EVs, while quotas were set for the number of imported gas cars that could be registered any given year.

Additionally, there was existing synergy China could exploit. Chinese EV success was predicated on earlier successes in battery manufacturing. BYD actually was founded in 1995 as a battery manufacturer, as part of a state-directed initiative that saw batteries as a core strategic component. The pattern here is similar: China deployed almost $100 billion in the industry to subsidize scale-up, and used import controls to artificially create early demand.

Chinese companies initially focused on lithium-iron-phosphate (LFP) chemistry rather than the previously dominant nickel-manganese-cobalt (NMC) for two reasons: LFP was largely untouched by Western companies, and Chinese companies controlled most of the supply chain for LFP batteries. This allowed them to expand rapidly on the lower-end of the market. Korean and Japanese companies had a long history in NMC for customer electronics. Success in LFP gave China advantages in scale and manufacturing process knowledge, that allowed them to expand into that contested NMC market and in general, higher-end EVs.

This state-directed industrial policy created China’s version of the Korean chaebol or Japanese zaibatsu: a vertically integrated corporation that dominates entire segments of the economy. BYD, now the world’s largest EV producer, started in batteries as discussed above.

Comments

No comments yet. Start the discussion.